A View from the Bridge - February 2017

So, the fingers are on the triggers and we are ready, steady and all set to go with the UK about to trigger Article 50 and the US Fed set to trigger the next interest rate rise. What that could mean for both economies will clearly play itself out over the coming months and years but there are already signs of divergence in the outlook for both.

In the US, the promise of tax cuts, infrastructure spending and the proposed repeal of certain financial regulation (Dodd Frank) has propelled the Stock Markets to almost daily highs. With core inflation rising to 2.5%, jobs growth of 227k for January and US house sales hitting a 10 year high, it is not surprising that Janet Yellen said to Congress in February that the Fed was “on course” to raise rates and the market expectation of a March rate rise is now 75%. Since President Trump was elected the long dated swap has risen sharply from circa 1.7% to 2.6%.

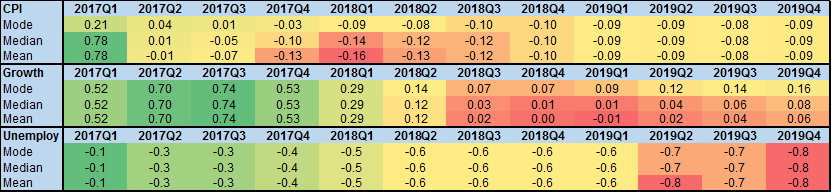

Meanwhile in the UK, despite the revision of the 2016 GDP figures downwards from 2% to 1.8% the outlook for 2017 remains at 2% and there is a slight uptick in the forecast for 2018 to 1.6%(1.5%) and for 2019 to 1.7% (1.6%). The Bank of England in its February inflation meeting forecast inflation exceeding the 2% target in Q1 2018 at 2.7% (2.8% in Nov) before dropping down to 2.4% by 2020. The implied movement in interest rates was revised upwards from the November inflation report by a year for Q3 2018 to Q3 2017 however the markets disagree and as at the end of February the expectation for a rate rise is back out to the end of 2018. The current 5 year swap rates v 3 month Libor are back down to 0.65% last seen in November last year.

In the Eurozone, Germany grew by 1.9% in 2016, knocking the UK off the top of the G7 GDP tables however with the likes of Greece shrinking by 0.4% the overall EZ growth rate remains at 0.4%. With 14 consecutive quarters of growth, unemployment below 10%, economic sentiment at a 6 year high and inflation increasing from 1.8% to 2% what could possibly go wrong for the Eurozone?

GBP short-term market interest rates again remained relatively static: 3mth closed at 0.36% (0bp) and 6mth closed at 0.51% (-2bp). Fixed Term rates (longer than 1 year) continued the recent see-saw, reversing all of last month’s gains to end lower: 5 Years closed at 0.79% (-25bp), 10 years closed at 1.18% (-28bp), 20 years closed at 1.44% (-26bp) and 30 years closed at 1.42% (-25bp).

UK Government Bond yields were also lower, 10 year UK Gilt Benchmark closed at a yield of 1.15% (-27bp) and the 30 year UK Gilt Benchmark closed at a yield of 1.74% (-31bp).

GBP future inflation expectations expressed through 20 year Inflation Swaps also ended lower, opening at 3.77%, with a high of 3.80%, low of 3.61% and closing 3.62%.

In the Foreign Exchange Market GBP was lower against the USD$ at 1.2380 (1.2579) and higher against the EURO at 1.1705 (1.1649)

PegasusCapital - 02/03/2017