A View from the Bridge - March 2026

As the protagonist said to Caeser in Shakespeare’s play “Beware the Ides of March” is particularly apt, following the convulsions in the interest rate markets after yesterday’s BOE decision, in what was the most volatile day since 2002. Twenty days into the Iran war and it’s severe impact upon energy supply via blocked shipping routes and refinery attacks has triggered a near 180-degree turn for the policy outlook, with most officials (including those with a previously dovish disposition) becoming concerned as to the potential for second round or persistent inflation following the surge in oil & gas prices and other byproducts (e.g. fertiliser and manufacturing alloys). In the immediate aftermath of the decision the market had moved to pricing three 25bp interest rate hikes by year-end, with a mild retracement to 2+ hikes by the close of business!

In many ways yesterday’s meeting should have been a calming influence on the market, and the Governor tried to emphasise that the economy is in a very different place to 2022 when excess demand after the pandemic lockdowns collided with a food and energy supply shortage triggered by Russia’s invasion of Ukraine, but the attacks on major LNG terminals in the early hours and another surge in prices put the market on the back foot. That said, Mr Bailey emphasised, as he did last month, that interest rates are much higher now [sic - with £100bn of QT as well] and with the outlook for growth and employment already weakening the upside threat to underlying inflation, it should be more muted once the initial impact of higher energy prices passes through.

Before this latest supply crisis there was little evidence of excess demand in the economy, as evidenced by subdued consumer spending and business investment, therefore increasing interest rates in response to higher energy prices would need more concrete evidence that second round inflation effects on wage demands were becoming likely, otherwise higher policy rates could cause additional harm to an already subdued business outlook (the complete opposite to the aftermath of the pandemic). We believe that current market pricing reflects a substantial uncertainty premium, in part caused by unwinding of previous trading positions expecting lower rates, alongside diminishing liquidity. The hurdle to a bank interest rate hike still feels quite high over the immediate policy horizon, not least because considerable uncertainty remains as to the duration of the war, whilst business sentiment, inflation surveys and pay settlements will be key drivers of the policy response over the next 6-9 months.

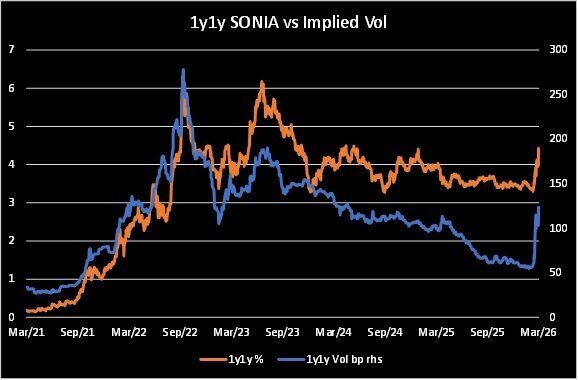

On February 27th the market was pricing 50bp of interest rate cuts to 3.25% by the November 5th meeting, but at close of business last night the market was pricing 65bp of hikes, a 115bp round trip! The options market was pricing just above 50bp of annualised volatility for 1- to 2-year SONIA rates, so we have seen realised volatility over 3x the annual implied in the space of three weeks. The 1-year inflation swap has increased by 190bp or 1.9% over the same period, implying a YoY CPI rate of 4.25% to December 2026. The 5-year inflation swap has increased by just over 60bp, primarily reflecting the1-year rise, suggesting that longer-term inflation expectations are not yet becoming unmoored.

PegasusCapital - 24/03/2026